Issue:

103

Page: 52-56

Sales of Herbal Dietary Supplements Increase by 7.9% in 2013, Marking a Decade of Rising Sales: Turmeric Supplements Climb to Top Ranking in Natural Channel

by Ashley Lindstrom, Carla Ooyen, Mary Ellen Lynch, Mark Blumenthal, Kimberly Kawa

HerbalGram.

2014; American Botanical Council

By Ash Lindstroma, Carla Ooyenb, Mary Ellen Lynchc, Mark Blumenthala, Kimberly Kawac

a American Botanical Council, Austin, Texas, USA

b Nutrition Business Journal, New Hope Natural Media, Boulder, Colorado, USA

c SPINScan Natural, Schaumburg, Illinois, USA

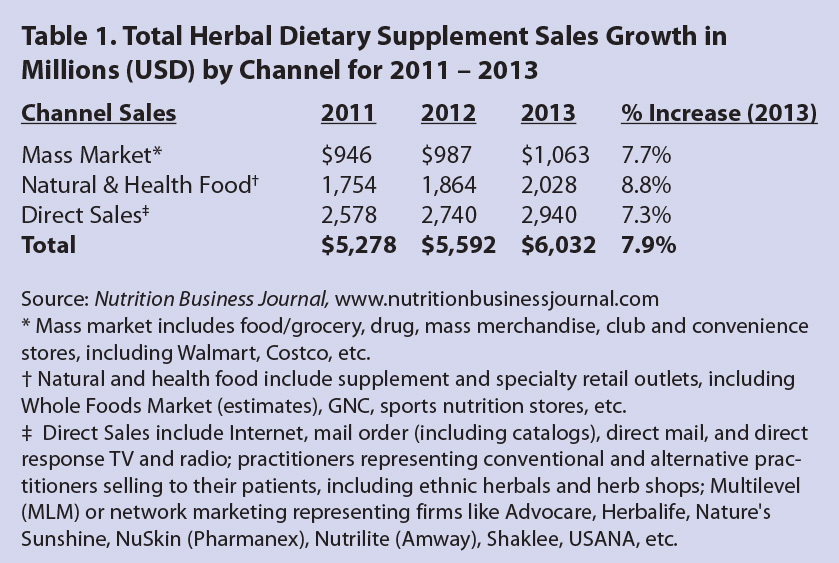

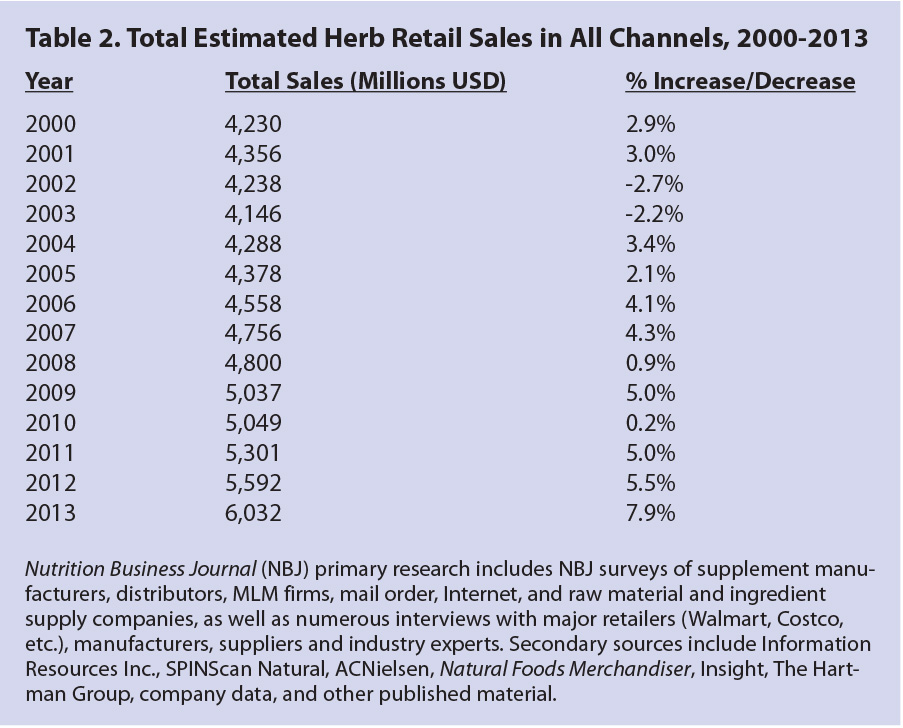

Total retail sales of herbal and botanical dietary supplements (DS) in the United States increased by an estimated 7.9% in 2013 — the highest observed growth percentage since the late 1990s — according to aggregated market statistics calculated by the Nutrition Business Journal (NBJ) (Table 1). The total sales growth is greater than the increase of 5.5% in total sales determined for 2012,1 marking the tenth year in a row in which herb sales in the United States have risen over the previous year (Table 2). These sales data did not include sales of herbal teas, herbs sold in natural cosmetic products, or herbs sold as government-approved ingredients in nonprescription medications (aka over-the-counter [OTC] drugs), e.g., senna leaf or fruit extract, or slippery elm bark.

Total 2013 herb supplement sales growth in distinct market channels varied, according to statistics provided by market research firms, from 7.7% over 2012 in the mainstream market channel to 8.8% in the natural and health food channel.

Mainstream Retail Channel

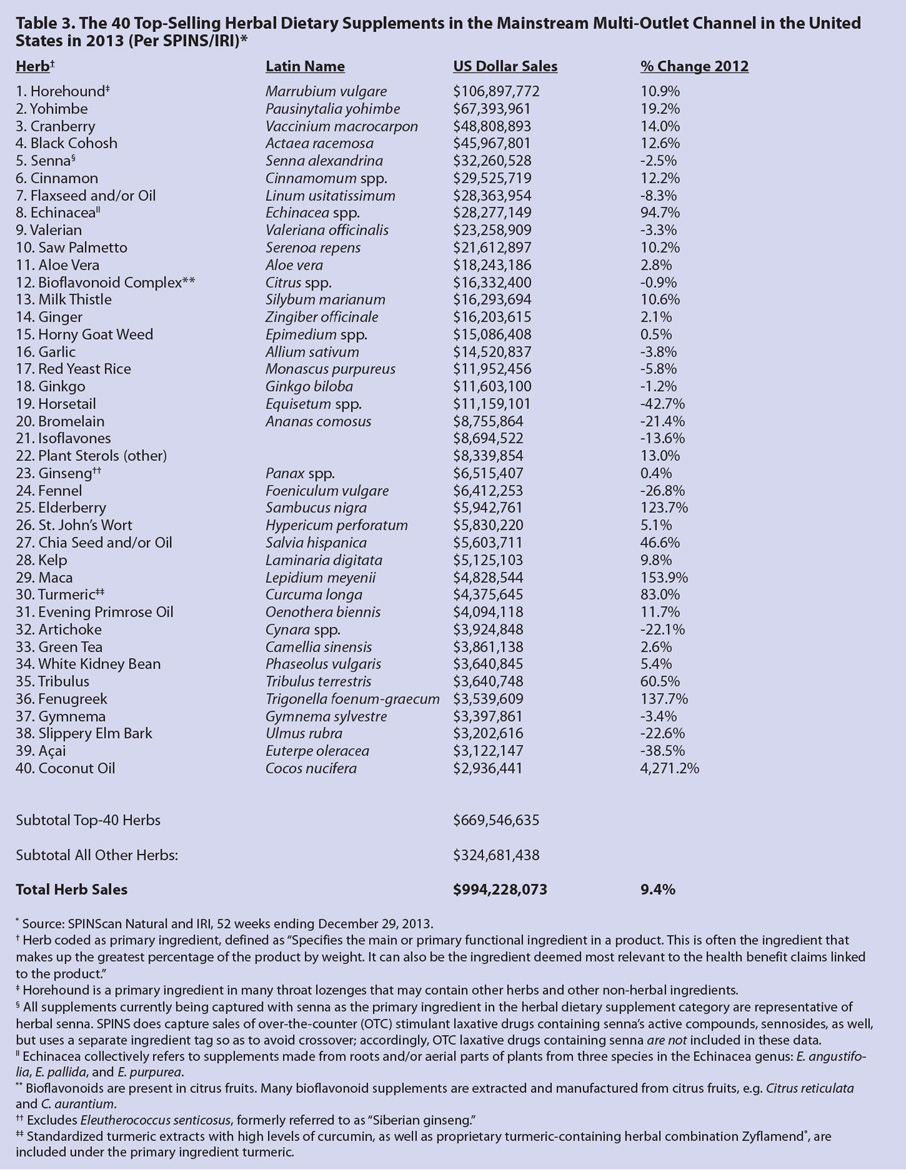

In the mainstream multi-outlet channel for 2013, an increase of 9.4% (with a sales total of $994,228,073) was calculated by SPINS and IRI, two leading market research firms that measure sales of consumer products in retail stores. In previous years, HerbalGram has featured separate mainstream sales data from the two firms, with SPINS calculating projections by applying its library to mainstream herbal dietary supplement sales data from Nielsen, another leading market research firm. For 2013, SPINS and IRI collaborated to present a combined report. This channel coverage includes the food, drug, and mass market sector (or “FDM”; supermarkets, drugstores, and mass market retailers), military commissaries, and select buyer’s clubs and so-called dollar stores. (The collaborative SPINS/IRI reporting does not include convenience store sales; sales data for such outlets are included in the NBJ total sales estimate.) The SPINS-IRI collaboration resulted in nuances in sales projections that make it of limited utility to reference specifically either set of 2012 data when viewing 2013 sales.

Though the popularity of many herbs remained relatively constant, the harmonization of product definitions that occurred during the collaboration did culminate in a few deviations and anomalies; for example, senna now appears among the top-five sellers. (Senna, known for its well-documented stimulant-laxative properties, may have developed a following among sedentary or aging Americans whose pharmaceutical medications affect bowel movement regularity, while its other uses deal with weight loss, digestive support, and bowel cleansing/detoxification programs.)

The sales increase in this channel illustrates continued mainstream acceptance of popular herbs including (alphabetically) black cohosh, garlic, ginger, ginkgo, ginseng, milk thistle, saw palmetto, St. John’s wort, and others. Notable herbs and plant ingredients gaining popularity in this channel include (alphabetically) coconut oil, fenugreek, gymnema, maca, and tribulus.

Coconut oil is a source of healthy fat and medium-chain triglycerides that has gained popularity among proponents of the Paleo diet. Traditionally, gymnema has been indicated for sugar and insulin regulation for conditions such as type 2 diabetes. Maca — a versatile South American tuber with a long history of safe use as a traditional food — may be administered in several forms and is claimed to have a breadth of benefits: for energy, reproductive health, sexual enhancement, menopause, and premenstrual syndrome. Tribulus is found in bodybuilding and sexual-enhancement supplements.

According to SPINS/IRI (Table 3), several herbs among their top 20 experienced notable increases in sales, particularly echinacea at 94.7%. Other top-20 herbs that exhibited relatively significant increases are black cohosh (+12.6%), cinnamon (+12.2%), cranberry (+14.0%), horehound (a primary ingredient in many throat lozenges; +10.9%), milk thistle (+10.6%), saw palmetto (+10.2%), and yohimbe (+19.2%).

Herbs showing remarkable increases in the top 21-40 rankings include chia seed/oil (a vegetable source of short-chain omega-3 fatty acids; +46.6%), coconut oil (+4,271.2%), elderberry (+123.7%), fenugreek (+137.7%), maca (+153.9%), tribulus (+60.5%), and turmeric (+83.0%; this is the first time turmeric has appeared among the FDM top-sellers rankings featured in HerbalGram over the past few years).

Of course, sales increases were not all-encompassing in this channel, with some herbs experiencing significant declines according to SPINS/IRI statistics. These include açai (-38.5%), artichoke (-22.1%), bromelain (a pineapple enzyme; -21.4%), fennel (-26.8%), and horsetail (-42.7%).

Sales figures for categories including “Chinese herbs,” “whole food concentrate,” “vegetable supplement oils,” and “herbal formulas (other)” were removed from the top-40 mainstream multi-outlet rankings by HerbalGram, due to their broadness. Biotin — a B vitamin sometimes sourced from plants — and Relora® (Next Pharmaceuticals; Salinas, California), a proprietary combination of magnolia bark and phellodendron bark extract, also were removed. Had these figures remained integrated, Chinese herbs would have appeared at #1, biotin and Relora at #21 and #22, respectively, whole food concentrate at #31, vegetable supplement oils at #38, and herbal formulas (other) at #39.

Overall, NBJ’s analysis for the total sales of herbal dietary supplements in the total mainstream/mass market channel (including estimated sales in buyers’ clubs [e.g., Walmart, Sam’s Club, Costco, etc.] and convenience stores) determined a slightly more modest increase of 7.7%.

Natural Channel

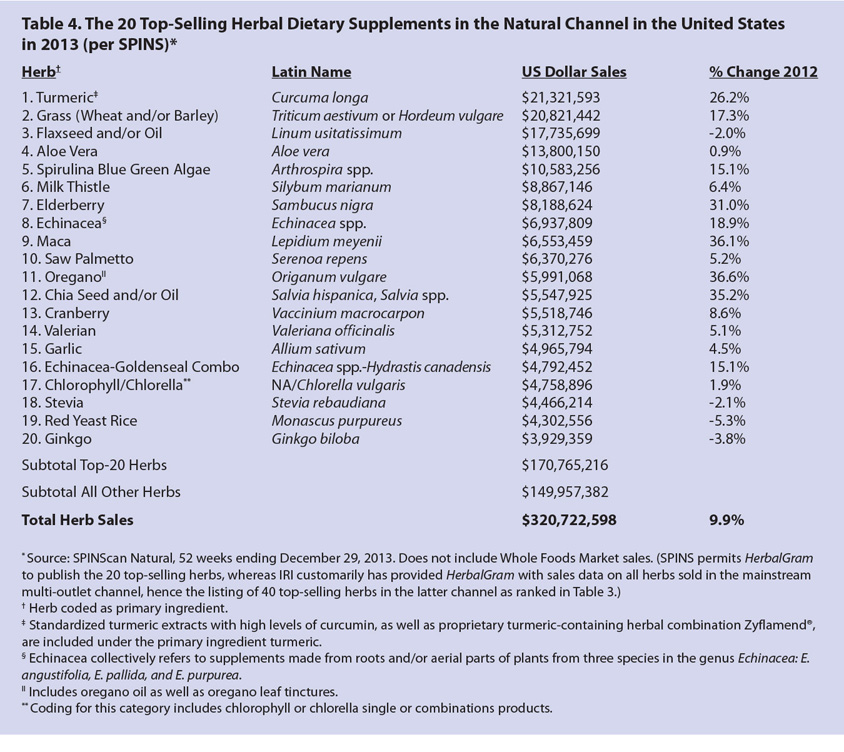

In the natural channel, total calculated sales for herbal supplements in 2013, according to SPINS, were $320,722,598 — 9.9% growth over 2012 sales (Table 4), which were considerable at a 14.7% increase over 2011 sales.2 (These data do not include sales data from natural foods retail giant Whole Foods Market, which does not report its DS sales to SPINS or other market tracking firms.)

In both the natural and mainstream channels, sales trends indicate strong growth among herbal supplements for energy, immune support, stress regulation (namely adaptogens), and Ayurvedic herbs. The so-called “Dr. Oz Effect” (the phenomenon of increased popularity of herbal dietary supplements featured on the television show of Mehmet Oz, MD), noted in HerbalGram’s 2012 herb market report, appears to be continuing to benefit natural channel sales of herbal dietary supplements. (There is a related story on Dr. Oz and his show’s impact on natural product sales in this issue on page 57.)

Typically, the natural channel is characterized by what some market experts refer to as “core shoppers” — those with a relatively strong commitment to a natural lifestyle, natural foods, and natural-health modalities — compared to the “peripheral shoppers” who have less of a personal commitment to natural foods, natural-health philosophy, and who purchase the majority of their dietary supplements in the mainstream channel.

Several key herbal supplements show evidence of significant growth in the natural channel. With a sales increase of 26.2% in 2013 (+39.8% in 2012), turmeric became listed as the top-selling herb primary ingredient in the natural channel. The primary ingredient “turmeric,” as compiled by SPINS, also includes herbal supplements of turmeric extracts containing relatively high levels of curcumin, the collective name for a group of key biologically active compounds in turmeric root and rhizome. Also included is the leading herbal combination supplement in the natural food market, Zyflamend® (New Chapter; Brattleboro, Vermont; containing quantities of, in descending order, extracts of rosemary, turmeric, ginger, holy basil, green tea, et al.), though the data from SPINS reports on mainly single-herb supplements. SPINS acknowledges that Zyflamend has been part of the turmeric sales compilation data in recent years, which may explain why turmeric has been ranked at #3 in sales in this channel for both 2011 and 2012. Collectively, manufacturer-claimed benefits for turmeric- and curcumin-containing herbal dietary supplements include joint health, liver focus, relief for pain/inflammation, cardiovascular health, and allergies.

Various greens showed noteworthy growth as well: spirulina blue-green algae (SPINS codes spirulina and blue-green algae supplements in the same category, with some combinations possibly represented; +15.1%) and wheat and/or barley grass (+17.3%). Also showing significant sales in 2013 are (alphabetically) chia seed/oil (+35.2%), echinacea (+18.9%), elderberry (+31.0%), and oregano (oil and leaf tinctures; +36.6%).

As noted above, sales compiled by SPINS for the natural channel do not include herb supplement sales in Whole Foods Market, the largest natural food grocer in the United States. Somewhat paradoxically, NBJ estimated a slightly smaller increase of 8.8% growth than the 9.9% reported by SPINS for herb supplement sales in the natural and health food channel in 2013, with its estimates attempting to include sales at Whole Foods.

Direct Sales

Sales of herbal dietary supplements in the direct sales channel include multi-level marketing companies (also known as network marketing companies, e.g., Advocare, Amway/Nutrilite, Herbalife, Nature’s Sunshine, Pharmanex/NuSkin, Shaklee, USANA, and others), mail order and Internet sales companies (e.g., iHerb, Indiana Botanic Gardens, Swanson’s, and others), and healthcare practitioners. As shown in Table 1, further demonstrating the vitality of the herbal supplement market in 2013, this channel experienced a 7.3% increase in growth over 2012 resulting in an increase of $2,940,000 in sales.

Single vs. Combination Herbal Dietary Supplement Sales

As shown in Table 5, estimates for sales of single-herb dietary supplements in all channels of trade increased by 5.1% in 2013, according to NBJ. (As shown, this category exhibited an increase of 2.7% in 2012.) Sales of combination formulations (usually marketed for a specific benefit, e.g., maintaining normal cholesterol levels, blood sugar levels, urinary tract and prostate health, etc.) continued to grow for at least the third straight year: In 2011, combination formulations were calculated at 34.5% of total herb sales; in 2012 they were 36.2%; and in 2013 combinations were estimated at 37.8% of total herb supplement sales. This growth represents an increase of 4.7% from 2011 to 2012, and 4.2% from 2012 to 2013, suggesting a continued increase in consumer interest in herbal supplements marketed for specific benefits.

Conclusion

The estimated 2013 herbal dietary supplement sales in all channels are illustrative of American consumers’ ongoing demand for botanical ingredients to integrate into their wellness and self-care practices. It should be reinforced that the sales discussed in this article pertain only to those involving herbal and other plant-based dietary supplements, and generally do not include herbs sold as teas and beverages, or as ingredients in natural personal care and cosmetic products, including so-called “cosmeceutical” products.

References

- Lindstrom A, Ooyen C, Lynch ME, Blumenthal M. Herb supplement sales increase 5.5% in 2012: herbal supplement sales rise for 9th consecutive year; turmeric sales jump 40% in Natural Channel. HerbalGram. 2013;99:60-65.

- Blumenthal M, Lindstrom A, Ooyen C, Lynch ME. Herb Supplement Sales Increase 4.5% in 2011. HerbalGram. 2012;95:60-65.

|