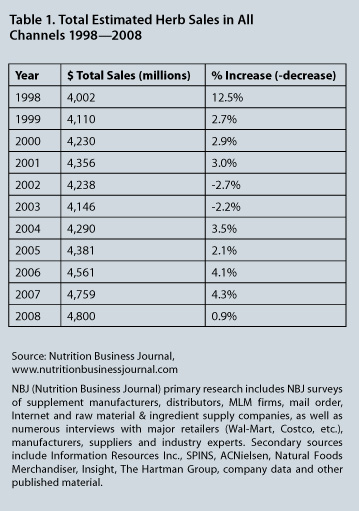

Sales of herbal and botanical dietary supplements in the United States rose slightly in some market channels in 2008, according to data gathered from market research firms. Information Resources Inc. (IRI) found steady growth of herbal supplement sales in the mainstream market channel,1 and SPINS has reported that botanical supplement sales remained relatively stable in the health and natural food stores sector.2 Nutrition Business Journal, meanwhile, has pooled various primary and secondary data sources and determined that total estimated herb sales in the US market rose by 0.9% in 2008 (see Table 1).

Herbal dietary supplements are sold in the United States through a variety of market channels, including health and natural food stores; food, drug, and mass market (FDM) retailers; warehouse and convenience stores; mail order, radio and television direct sales; Internet sales; network or multi-level marketing (MLM) companies; health professionals in their offices (e.g. acupuncturists, chiropractors, naturopaths, some conventional physicians); and other channels. While market data companies are able to generate relatively accurate data of herbal dietary supplement sales for some market channels through cash register and computer scanning records, most channels do not have such tracking capabilities and are estimated with a lesser degree of accuracy. However, by pooling various sources of available data and modeling the remaining multi-channel firms, NBJ has arrived at a total estimated figure for all US herbal dietary supplement sales in 2008 of $4,800,000,000.

According to data supplied by IRI of Chicago, Illinois, sales of herbal dietary supplements in the FDM channel increased by 7.16% in 2008 from 2007 sales, for a total figure of $289,248,200.1 However, the IRI data does not represent the entire FDM channel, as it does not include sales reports from Wal-Mart, Sam’s Club, and other large warehouse buying clubs, or from convenience stores. Based on data from a SPINSscan consumer report driven by Nielsen Homescan’s panel of 125,000 households, the market information firm SPINS of Schaumburg, Illinois, has estimated that Wal-Mart probably accounts for less than 9% of all herbal supplement sales in the United States.

Previous statistics from IRI found that sales of herbal supplements increased for the first time in the FDM channel in 2007, after showing steady decreases for several years.3 This year’s IRI data shows a continuing trend toward increased consumer purchasing of herbal supplements from mainstream market retailers.1 The 20 top-selling single herbal dietary supplements within the FDM channel, as determined by IRI, are listed in Table 2.

Sales of cranberry (Vaccinium macrocarpon, Ericaceae) supplements, which increased by more than 23% in 2007 from 2006,3 continued to rise in 2008, making cranberry the top-selling herbal supplement product within the FDM channel.1 As noted in last year’s HerbalGram article on the herb supplement market,3 a systematic review of 10 randomized controlled trials was published by the Cochrane Collaboration in January of 2008, concluding that cranberry products may prevent recurrent urinary tract infections in women.4 Such information, in addition to other studies on cranberry’s health benefits, may have contributed to the steady rising sales of cranberry supplements. Sales of elderberry (Sambucus nigra, Caprifoliaceae) and ginger (Zingiber officinalis, Zingiberaceae) supplements made significant strides in the FDM channel in 2008, whereas sales of yohimbe (Pausinystalia johimbe, Rubiaceae) supplements appear to have dropped rather sharply.1

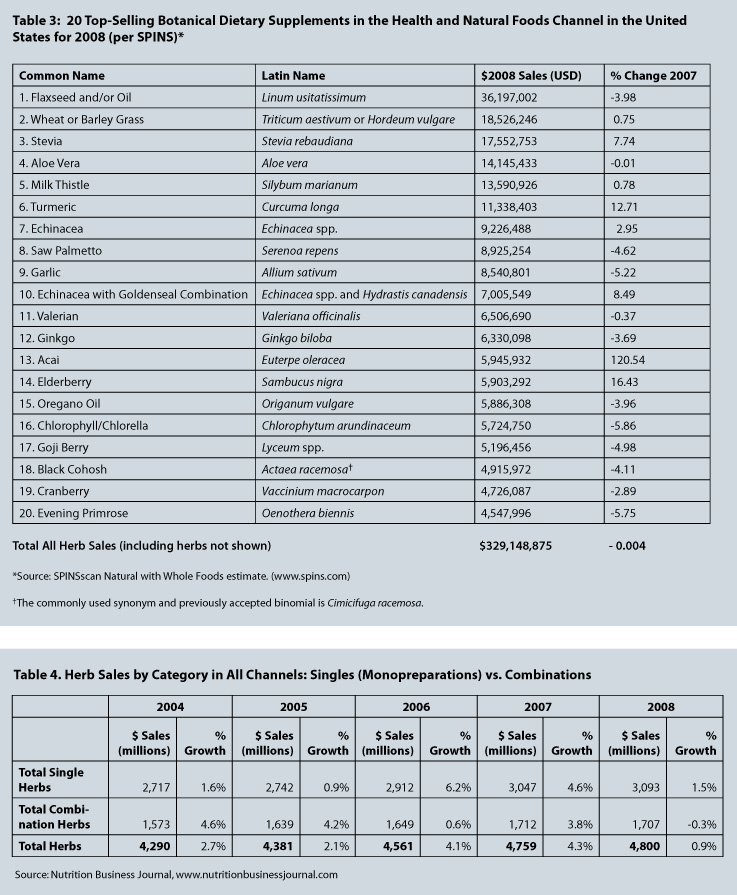

Natural and health food stores typically provide a larger share of the herbal/botanical supplement market than FDM outlets, since they tend to cater to what are frequently referred to as “core” shoppers, i.e., consumers who are aligned with the values of the natural products market. SPINS has determined that sales of botanical dietary supplements in the natural and health food channel—including estimated sales from the natural foods retailer Whole Foods—decreased minutely by 0.004% in 2008 from 2007 sales, for a total of $329,148,875.2 SPINS collects data on supplement sales from a variety of natural and health food retailers. Although Whole Foods no longer reports its sales to SPINS, the market information firm is able to estimate sales of supplements from Whole Foods using an algorithm that incorporates historical point of sale data, industry trends, Whole Foods’ quarterly financial reports, and other factors.

The 20 top-selling botanical dietary and food supplements within the natural and health foods channel, as determined by SPINS, are listed in Table 3. According to SPINS, flaxseed (Linum usitatissimum, Linaceae) and flaxseed oil products were the top-selling botanical supplements within the natural and health foods channel. Steady interest of consumers in sources of omega-3 fatty acids may be the cause behind this supplement’s high sales. The superfruit supplement acai (Euterpe oleracea, Arecaceae), meanwhile, showed a particularly significant increase in sales from 2007.

The sweetening-agent stevia (Stevia rebaudiana, Asteraceae) was also a top-selling botanical supplement in 2008, and its sales increased from the previous year. Future data, however, may show decreased sales of stevia as a supplement, due to recent introductions of mass market brands of stevia as food additives. As was reported in HerbalGram issue 81, 2 companies received notice from the US Food and Drug Administration in December of 2008 that the agency would not object to the use of the companies’ stevia preparations as food substances that are generally recognized as safe (GRAS).5 Other companies that produce and market stevia are reportedly seeking and may receive similar FDA acceptance for their respective preparations, meaning that sales of stevia as a supplement may decrease as sales of stevia as a sweetener increase.

It bears emphasis that various market research companies use different definitions and coding techniques to compile and analyze data on a particular topic. Therefore, data from IRI on botanical supplement sales in the FDM channel and data from SPINS on botanical supplement sales in the natural and health foods channel—though both considered reliable statistics and important for understanding the herbal market—may not be directly comparable. The 2 market research firms categorize products differently and do not necessarily include the same products in their data of herbal supplement sales. For example, some of the leading products noted by SPINS as top-selling botanical supplements (including flaxseed and stevia) are not classified as individual herbal supplements in IRI’s data for the FDM channel. Likewise, NBJ’s total estimated figure for herbal supplement sales may include or not include some herbal/botanical supplements contained within the data of IRI and/or SPINS.

Sales of single herbal dietary supplements experienced growth in 2008, whereas sales of combination herbal supplements decreased slightly, according to data from NBJ (see Table 4). Sales of single herbal dietary supplements (monopreparations) grew by 1.5%, while combination herbal supplements decreased by 0.3%. Monopreparations typically pull in almost twice as much in sales as combinations.

NBJ data also indicates that herbal supplement sales increased in the mass market and natural foods channels but decreased in the direct sales channel (see Table 5). According to NBJ, herbal dietary supplement sales increased in the FDM channel by 6% in 2008 over 2007 sales (and this figure does include sales from Wal-Mart, club warehouses, and convenience stores). The natural and health foods channel increased slightly by 1.5%, and the direct sales channel decreased slightly by 1%. According to NBJ, early indications suggest that slower growth in superfruit supplement sales in 2008 led to the decrease in the direct sales channel, as well as flat to slightly negative sales growth in US sales from publicly traded MLMs. (NBJ’s figures on growth in the FDM and health and natural foods channels differ from IRI and SPINS primarily because NBJ estimates and includes other retail channels not tracked in IRI and SPINS data.)

Some retailers and market research firms have indicated that sales of herbal supplements may have risen significantly in the last quarter of 2008 and into 2009, due to the economic recession.6 As consumers are faced with growing financial concerns and budget restraints, selected herbal dietary supplements may continue to become substitutes for the more costly conventional pharmaceuticals, particularly among many of the millions of consumers without health insurance. Market statistics from the first and second quarters of 2009 should provide further evidence as to whether the nation’s financial downturn results in increased sales of herbal supplements.

References

- FDM Market Sales Data for Herbal Supplements, 52 weeks ending Dec 28, 2008. Chicago, IL: Information Resources Inc.

- SPINSscan Natural, $2mm+ Natural Supermarkets with Whole Foods estimate sales data, Total US, 52 weeks ending December 27, 2008 and year ago, SPINS defined herbal category.

- Cavaliere C, Rea P, Blumenthal M. Herbal supplement sales in United States show growth in all channels. HerbalGram. 2008;78:60-63.

- Jepson RG, Craig JC. Cranberries for preventing urinary tract infections. Cochrane Database of Systematic Reviews. 2008:Issue 1.

- Cavaliere C. FDA accepts safety of two stevia preparations for food and beverage use. HerbalGram. 2009;81:67-69.

- Tanner L, With economy sour, consumers sweet on herbal meds. Associated Press; January 13, 2009.