Issue: 90 Page: 64-67

Herb Sales Continue Growth – Up 3.3% in 2010

by Mark Blumenthal, Ashley Lindstrom, Mary Ellen Lynch, Patrick Rea

HerbalGram. 2011; American Botanical Council

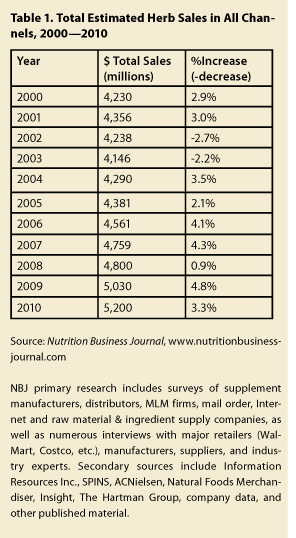

The herbal dietary supplement (DS) market increased in sales in the United States in 2010 over 2009, continuing a steady growth trend since 2003 despite the continued relatively weak economic conditions in the United States and elsewhere in the world. Total herb DS sales in all channels of retail trade increased by an estimated 3.3 percent according to the Nutrition Business Journal (NBJ), which, along with SPINS, a market research firm specializing in natural product sales, collaborated with the American Botanical Council to produce this annual report in HerbalGram. Although the rate of growth is less than the 4.8% growth rate from 2008 to 2009, this increase perpetuates the trend of positive growth for herbal DS during 9 of the past 11 years (per Table 1).

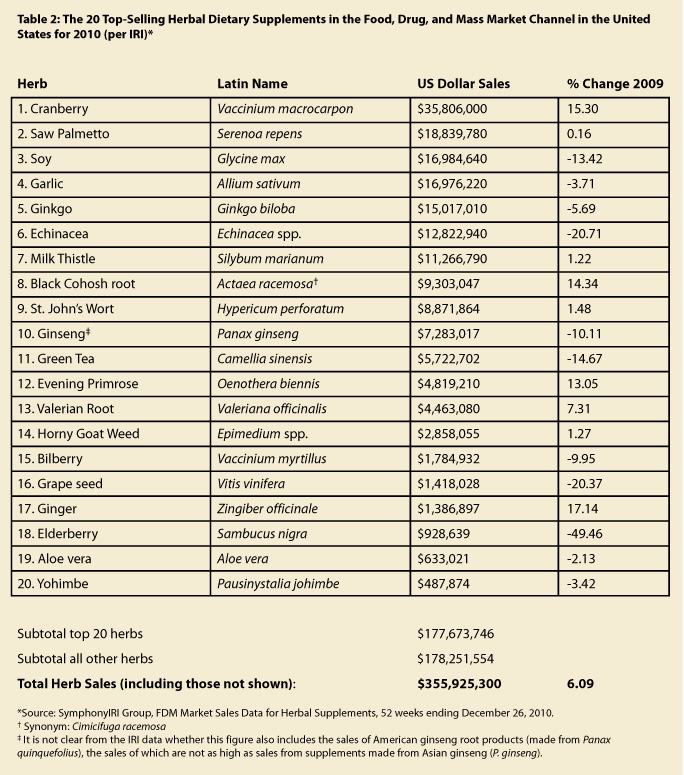

In the Mainstream Food, Drug, and Mass Market (FDM) channel (drugstores, grocery stores, mass market retailers, et al., but not including Wal-Mart), the degree of increase varies depending on the source of the sales information. Total single-ingredient herbal DS sales in the FDM channel rose by 6.1%, according to Symphony IRI (Table 2), and SPINS FDM powered by Nielsen, a leading provider of market information (data not included in tables), calculated an increase of 4.8%. However, unlike IRI, the SPINS/Nielsen FDM datacollection parameters include combination herbal dietary supplements, with primary ingredients chosen to represent certain products (per the discussion of horehound below).

As an example of the complexity of any analysis of this segment, NBJ’s analysis for the total sales of herbal DS in the mainstream/ FDM channel (including estimated sales in buyers’ clubs and convenience stores, including Wal-Mart, Sam’s Club, Costco, et al.) shows that herbal DS sales grew at a higher rate than those reported by IRI or SPINS/Nielsen, i.e., an NBJ-calculated increase of 6.6%, from an estimated $878 million in 2009 to $936 million in 2010.

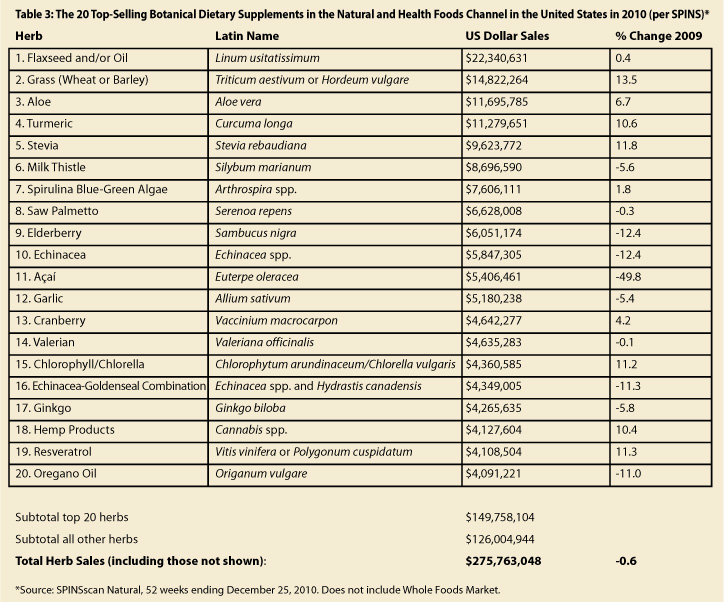

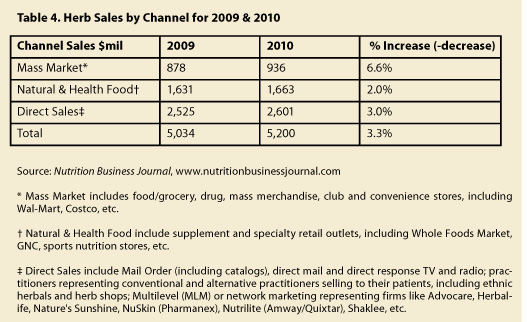

Per Table 3, SPINS has calculated that total herb DS sales in the Natural Products channel decreased by an estimated 0.6% (not including sales in Whole Foods Markets). NBJ, using that SPINS information supplemented with estimated sales from GNC and Whole Foods Market, calculates a total increase of 2% for the Natural channel, with total sales increasing from an estimated $1.631 billion in 2009 to $1.663 billion in 2010 (Table 4).

The increase in overall herbal DS sales is also reflected in other channels of trade, e.g., the Direct Sales channel (including mail order, Internet, MLM [multi-level marketing], etc.) where sales increased in 2010 by an estimated 3% according to aggregated market data compiled by NBJ, from $2.525 billion in 2009 to $2.601 billion in 2010 (Table 4).

In all previous years since HerbalGram began to report on herb sales in the FDM market in the 1990s, the data were derived from reports provided by Information Resources, Inc., a Chicago market research firm now known as Symphony IRI. This year, for the first time, the Herb Market Report was also able to access FDM sales data from SPINS powered by Nielsen via the ABC collaboration with SPINS. Both SPINS FDM and Symphony IRI FDM sales exhibit an upward trend, though that trend varies in degree of magnitude, as noted previously. Again this underscores the ongoing and significant challenge of collecting and deciphering herbal product sales information.

“SPINS is focused on meeting the information needs of the Natural and Health & Wellness Industry and uses an internal team of Natural Product Experts to insure detail coding of ingredients to support those needs,” said Kerry Watson, SPINS coding library manager (e-mail communication, April 26, 2011). “The information provided to HerbalGram for use in this analysis is limited to botanical-based supplements and does not reflect sales of food and beverages.”

Of interest is the actual determination of herbs that are in the top 20 in sales as compiled by Symphony IRI and SPINS FDM powered by Nielsen. While it is understandable and predictable that the rankings and inclusion of herbs would vary in the Natural channel compared to the FDM channel (as noted elsewhere in this article), it is noteworthy to see “Horehound” (Marrubium vulgare, Lamiaceae) as the top-selling individual herbal DS in the SPINS FDM rankings—reportedly generating $68.0M in sales in 2010! This raises the question as to whether ABC should be stating that horehound is one of the top-selling herbs in the United States, a statement that would probably be met with considerable curiosity, if not skepticism, by many market veterans.

Horehound has never been listed as a top-selling herbal supplement in any previous HerbalGram Herb Market Report in either the FDM channel (as measured by IRI) or the Natural Products channel. Digging deeper, SPINS revealed that this herb is the primary ingredient in several Ricola® cough or throat drops, which are sold as dietary supplements. According to 2008 and 2009 SPINS FDM powered by Nielsen data, within their data-collection parameters, horehound sales—which include the Ricola products for which SPINS assigned horehound as a primary ingredient, and other dietary supplement products for which SPINS identified horehound as the main (or only) ingredient—have been significant and showing a trend of growth, bringing in a total of $58.7M in 2008 and $64.7M in 2009.

Horehound is a well-known folk remedy for sore throats, but there has been little modern research on this herb and ABC is unaware of any published clinical trials supporting its efficacy for cough or for soothing a sore throat.

It is worth noting that the top-20 best-selling herbal supplements in the mainstream/FDM and Natural Products channels (per Table 2) include many traditional and conventional food items; there are at least 8 foods in the FDM channel; in sales ranking, these include cranberry, soy, garlic, green tea, ginger, bilberry, grape seed, and elderberry. There are at least 10 food herbs in the Natural channel (i.e., depending on how one evaluates some of these ingredients as foods); in ranking of sales, these include flaxseed, wheat or barley grass, turmeric, spirulina algae, elderberry, açaí, garlic, cranberry, chlorophyll, and oregano oil (Table 3). This popularity of food-based herbs is indicative of the fact that many popular herbal supplements are not exotic or arcane medicinal ingredients but have been used for centuries (and millennia) as foods and spices (e.g., garlic, ginger, oregano, turmeric). (Note: In some Asian countries, e.g., China and Korea, cultivated ginseng root, appearing annually as a top-seller in the FDM channel but not in the Natural channel, is frequently eaten as a food item and is a popular everyday beverage for millions of people.)

Further, the top-ranking sales of single herbal DS in both the FDM and Natural Products channels represents a long-noted trend of consumer interest in many of the more well-researched herbs which have become relatively well known due to a growing body of scientific and clinical research conducted on them. These include the following, as noted in order of ranking for sales in the FDM channel (Table 2): cranberry, saw palmetto, garlic, ginkgo, echinacea, milk thistle, black cohosh, Asian ginseng, green tea, etc.

Changes in 2010

Probably the greatest change in herb sales in the United States in 2010 compared to the 2009 market is the fact that by 2010, the worldwide concern prevalent in 2009 about potential pandemics related to infections from the H1N1 flu virus abated—to the point that public health discussions on this topic were noticeably absent. Thus, the spikes in sales in herbs that are perceived to be useful to prevent or treat symptoms of any type of flu based on traditional use and/or modern research did not occur. The sharp increases in 2009 sales for echinacea and elderberry supplements, for example, did not continue in 2010 and these 2 herbs actually experienced a predictable drop in sales as they reset to levels that would be consistent prior to H1N1 concerns. Sales for echinacea supplements dropped 20.7% in FDM and 12.4% in the Natural Products channel while elderberry sales decreased 49.5% in FDM and 12.4% in the Natural Products channel (Tables 2 and 3).

Hemp supplements have made their debut in the top-20 in the Natural Products channel, according to SPINS—a potential harbinger for future trends in other channels. “Hemp products” now rank 18th in sales in this channel, with over $4 million in total sales (Whole Foods Market sales not included), up over 10% from 2009. The growing popularity of hempseed (from non-psychoactive Cannabis sativa, Cannabaceae) as a high-protein, high omega-3 fatty acid-containing food item has undoubtedly migrated to growing consumer awareness of the potential nutritional benefits of hempseed oil sold as a DS in soft-gelatin capsules. When the growing popularity of this ingredient will migrate to the mainstream FDM channel remains to be seen.

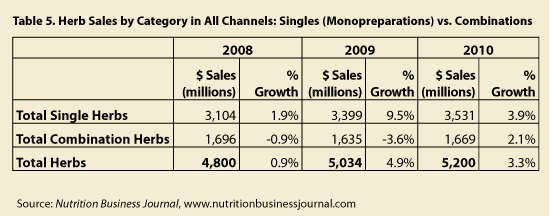

As noted in Table 5, estimates for sales of single herbal DS in all channels of trade increased by 3.9% in 2010 over 2009, according to NBJ. This compares to a larger increase of 9.5% in 2009 over 2008. Sales of combination formulations (usually marketed for a specific function or benefit, e.g., maintaining normal cholesterol levels, normal blood sugar levels, urinary tract health, etc.) increased 2.1% in 2010 compared to 2009, the first increase in sales of combinations since 2007.

In sum, the herb market in 2010 maintained the robust growth seen in recent years, reflecting increasing consumer interest in good nutrition and natural lifestyles.

|